In India, many people believe that becoming rich is not possible. Most of them lack a clear understanding or approach to investing and just follow the usual path, such as saving only in fixed deposits, frequently buying things on EMI, or spending without a proper budget. In this blog, we will see how to break free from this “middle-class” trap.

Step 1: Cut Down Expenses and Build Financial Habits

1. Track All Expenses: Always keep track of all your expenses—every single one, including small purchases like sweets, chocolates, a party expense, or weekend movies.

2. Cut the Extras: Identify and cut out the extra expenses that could have been avoided, such as ordering food from outside when food is available at home.

3. Reduce and Save: Start small, even if it is 1%, and redirect that amount into savings. For example, if monthly expenses are 50,000 rupees, 1% of that, which is 500 rupees, ca be achieved by skipping just one Swiggy order.

4. Power of Habit: The initial savings amount might seem small, but what is more important is to cultivate that habit and be consistent

Step 2: Build the Safety Net

1. Establish an Emergency Fund: Many people who do not save regularly may not be able to provide for emergencies such as a job loss. The first practical step is to build an EMERGENCY FUND that will last at least 6-12 months.

2. Do the math: Determine your monthly expense (e.g., 30,000 rupees) and multiply it by six months, which will be around 1.8 lakhs. This resulting number should be held in cash, in your savings account or highly liquid safe debt funds.

3. Secure Health Insurance: Financial health is also threatened by health emergencies. Most people do not become poor because they made less money; they become poor because one single event puts them behind. Given that health expenses are becoming very high, having health insurance is crucial alongside an emergency fund to ensure that you are safe.

Step 3: Controlling Debt

- Avoid show-off: People often follow the herd and buy things they cannot afford just to fit in with society. Purchases like an iPhone, a car, or a house have become a status symbol, thereby driving businesses to take advantage of this mindset. This eventually puts people in a vicious cycle that we call debt!

- Understand the Cost of Debt: Every EMI you pay doesn’t just buy you the product. The bank or credit card company owns it until you settle it fully. The real cost isn’t money alone; it’s your time and effort you put into earning that money. You are working hard to pay them rather than letting your money grow.

Step 4: Start Investing

- Begin Early: You don’t need a huge corpus to start investing. Even a small amount like Rs. 1000 is enough to build the habit of investing. The key is to start- start early, stay consistent and let the compounding do the magic.

- Let’s Visualise It:

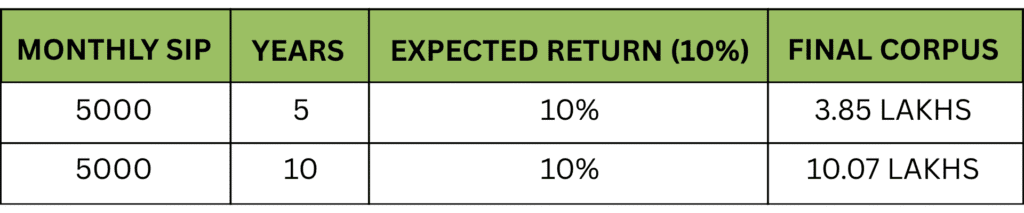

Let us take an example to see how a Rs 5000 SIP in a mutual fund earning 10% grows in 5 vs 10 years

Scenario 1: Short-term

Your total investment of Rs. 3,00,000 over 5 years will grows to Rs. 3.85 Lakhs. This is just a meaningful growth for staying consistent

Scenario 2: Long-term

The same Rs. 5000 SIP in 10 years will grow to Rs. 10.07 lakhs. Here we can see how compounding plays a major role in your wealth creation journey.

So, every time you get out of any of the debt, instead of thinking about taking on another loan, just think about investing in the growing assets.

Conclusion:

Getting yourself out of the middle-class trap isn’t just about earning a lot of money. It’s about changing habits, thinking big and letting the money work for you. In this blog, I have shared some practical steps, from tracking your expenses, building safety nets, to controlling the debt and investing benefits. Turn small and consistent actions into building long-term wealth. The goal is simple: start today, stay disciplined and be free from the middle-class trap.