Businesses where the parent sits outside of India, where the brand was built decades ago, and where the dividend arrives with clockwork reliability regardless of what the broader market is doing, deserve a second look.

Called MNCs, these businesses are characterised by structurally superior financial metrics versus the broader market:

- Return on Equity (ROE): Most portfolio constituents sustain ROE above 20% through business cycles — a reflection of asset-light models, brand moats, and parent-backed IP.

- Debt-free or near-zero-leverage balance sheets: FMCG and industrial MNCs in India carry light financial debt, creating earnings resilience during rate tightening cycles.

- Dividend yield: The Nifty MNC index historically delivers an approximately 3% dividend yield — significantly above the Nifty 50’s typical ~1.2%.

- Valuation premium: MNC stocks have traded at structurally elevated multiples, with the Nifty MNC P/E averaging 28–35x historically.

Today, the bull case for MNCs rests on two structural pillars. First, India’s per-capita income trajectory. As the economy moves from the $2,500 GDP per capita (2023) to $5,000 GDP per capita (2032-2033) (Source: World Bank, IMF consumption studies on emerging markets) discretionary and premium consumption spending will pick up. MNCs with strong brand equity and distribution are structurally positioned to benefit from this trend.

Secondly, with SEBI’s restriction on fresh inflows into international mutual fund schemes (the USD 1 billion AMC-level cap for overseas ETFs was hit by April 2024), MNC mutual funds have emerged as a proxy for global corporate exposure — investing in Indian-listed subsidiaries of global giants like Nestle, Unilever, Siemens, and Honeywell. This narrative has supported incremental flows into the category.

MNC Funds

MNC funds are classified as Thematic Funds under SEBI’s equity scheme framework, mandated to invest at least 80% of assets in equity and equity-related instruments of a defined theme. The theme here is ownership: investible companies must have foreign promoter shareholding exceeding 50%. This is not a sector filter. It is an ownership and governance filter that cuts across FMCG, capital goods, pharma, automobiles, specialty chemicals, and technology simultaneously.

How Funds Differ

Not all MNC funds are built the same. The category is dominated by three legacy funds from SBI, ABSL, and UTI. ICICI Pru has gained notable traction in AUMs (assets under management) despite launching only in 2019. Beneath the shared mandate lies meaningful variation in active positioning:

SBI Magnum Global — The oldest and largest, carries a more diversified approach including specialty chemicals (Aether) and healthcare alongside the core FMCG-auto blend. Lower portfolio concentration.

UTI MNC Fund — Higher turnover (~41%), slightly more willing to rotate into value pockets within the MNC universe (Vedanta, United Spirits). More contrarian.

ICICI Prudential MNC Fund — Has the highest cash allocation (7–8%) among peers, suggesting a more selectivity-driven approach. Overweight on healthcare relative to peers.

Aditya Birla SL MNC Fund — Is the longest-running active MNC fund (since Dec 1999). More conservative active share, lower turnover (~19%). Returns broadly in line with benchmark — arguably the most index-like of the active funds.

Across the fund universe, MNC portfolio holdings cluster into five main sector groupings:

- Consumer Staples (FMCG): Dominant across all funds — HUL, Nestle India, Britannia, P&G Health, Colgate-Palmolive. They feature high ROE (often 30%+), near-zero debt, reliable dividends. These stocks form the core of the governance premium argument.

- Consumer Discretionary / Automobiles: Maruti Suzuki, Hyundai Motor India (post-2024 listing). Cyclical, but backed by global R&D capability and strong balance sheets.

- Healthcare / Pharma: Divi’s Laboratories, Sun Pharma, Abbott India, Sanofi. Significant in ICICI Pru and SBI.

- Industrials / Capital Goods: Siemens, ABB, Honeywell Automation, Cummins India. Highly cash-generative, asset-light relative to Indian PSU counterparts — and direct China+1 beneficiaries.

- Specialty Chemicals / Basic Materials: Aether Industries (SBI), Vedanta (UTI, ICICI Pru). The most contrarian/value-oriented allocations — and the ones that differentiate most from the Nifty MNC TRI.

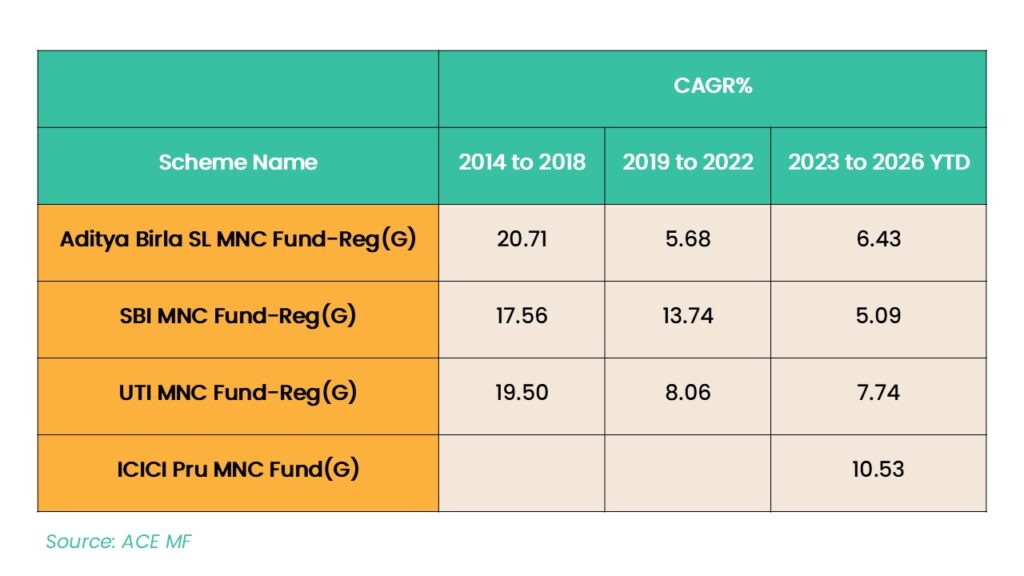

How Are They Faring?

The cycle-by-cycle lens in the accompanying table draws key observations. All three legacy funds delivered 17–21% CAGR between 2014-2018. This was the golden era for MNC funds — India’s consumption story was being discovered, FMCG premiumisation was accelerating, and governance-quality stocks were being re-rated. 2019-2022 saw a dramatic shift. This period saw credit crisis, a pandemic crash, a recovery where cyclicals particularly PSUs led that rally and FMCG lagged badly which led to MNC funds delivering poor returns. We are now entering a period that looks a lot like early Cycle 1 — post-correction phase, consumption inflecting, governance premium widening. If that thesis plays out, all funds should re-rate.

Current Positioning

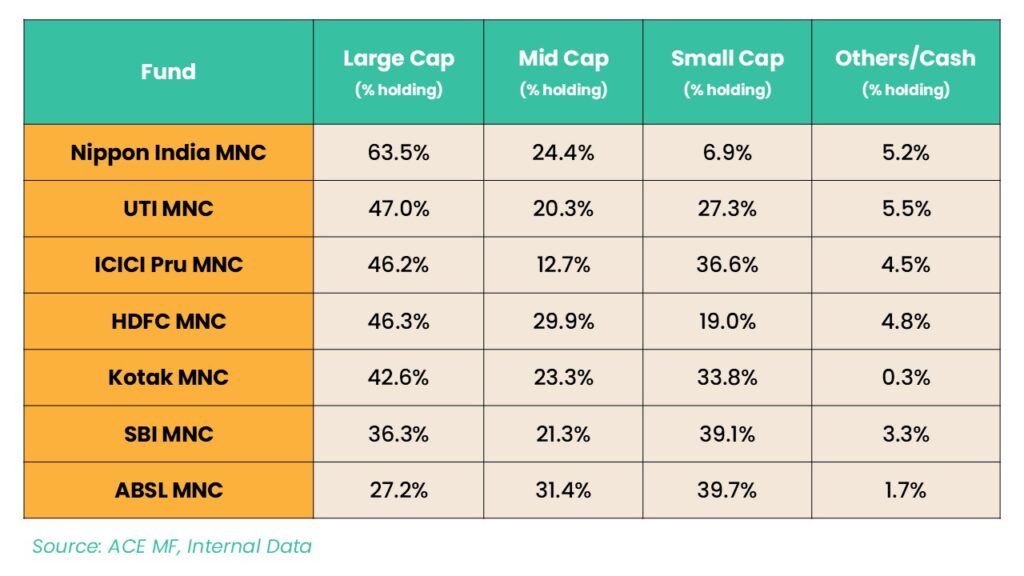

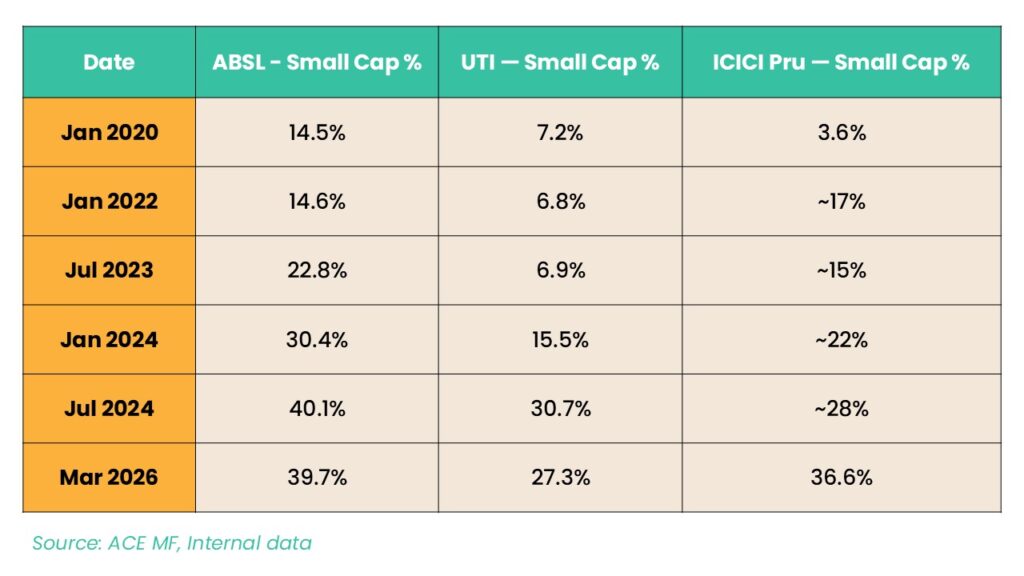

The market-cap allocation data for March 2026 across funds reveals an important insight : funds are now running significantly more small-cap exposure

The shift in small-cap exposure over 2023–2024 is not random drift — it is one of the most significant trends. Both ABSL and UTI approximately doubled their small-cap allocation

ICICI Pru’s large-cap exposure compressed from 61.6% (Jan 2020) to 46.2% (Mar 2026) while small-cap grew from 3.6% to 36.6% — a near 10x increase over six years. This is active portfolio repositioning with ABSL, SBI, and ICICI Pru are meaningfully more small-cap intensive.While the10–14% YTD 2026 drawdowns in these funds partly reflect this small-cap exposure under market stress, it also reflects the opportunities to invest in, for the long-term. Investors looking to invest in high quality small and midcaps can explore this category.

While the case for MNC funds is strong, risks need to be considered too:

Risk 1: Structural Underperformance in Momentum/Cyclical Markets

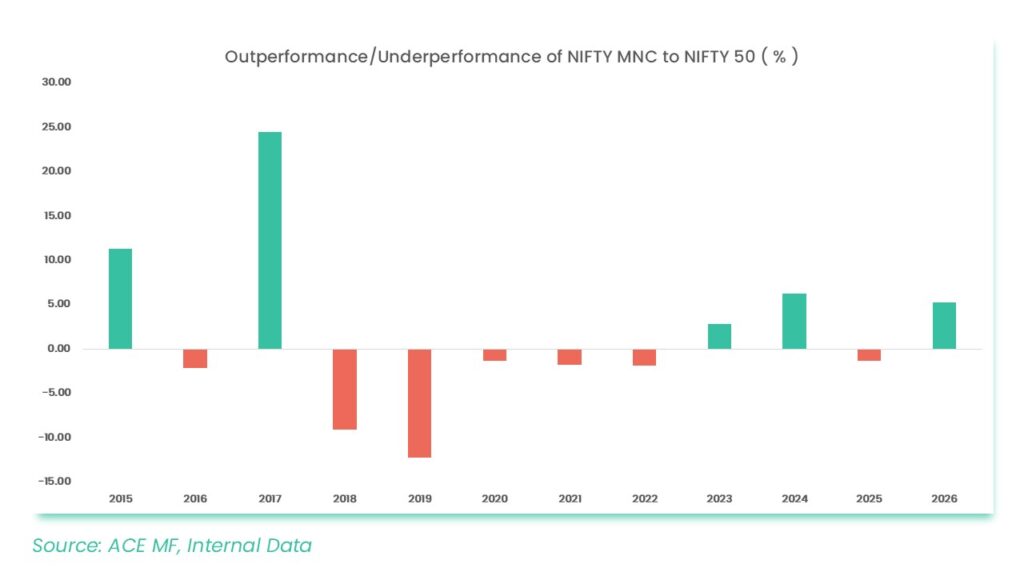

MNC funds are not momentum vehicles. During broad risk-on rallies driven by domestic cyclicals, PSUs, infrastructure, or broad small-cap momentum — 2018–19, 2021, and much of FY24 — MNC funds lag significantly. If your horizon is under 5 years, this category will test patience precisely when other themes are generating excitement.

Risk 2: FMCG Slowdown

A large share of MNC fund portfolios sits in consumer staples companies that faced sustained rural volume pressure and premiumisation challenges through FY24–FY25. HUL, Nestle, and Britannia collectively form a large portion of both the index and active fund portfolios.

Risk 3: Valuation Risk

MNC stocks trade at premium P/Es historically. This premium reflects governance quality and earnings consistency. The current Nifty MNC PE at approximately 35.5x is below the 5-year median of 44x. Entering on the wrong side of a valuation cycle can lock in years of sub-benchmark performance even in fundamentally sound businesses.

Risk 4: High Small-Cap Exposure

ABSL and SBI are now running 39–40% small-cap allocations — fundamentally changing their risk profiles. Investors who entered these funds expecting a large-cap FMCG-dominated defensive portfolio may be surprised by the drawdown behaviour during small-cap sell-offs.

Risk 5: Global Parent Risk — Not a Free Lunch

Decisions at the parent-company level — strategic pivots, profit repatriation, delisting attempts (eg. Linde India 2024 case), or scaling back India operations — can materially impact listed Indian subsidiaries.

Who Should Invest

- Investors seeking to capitalise on India’s domestic consumption and manufacturing story

- Investors who prefer businesses with strong governance, clean balance sheets (low or no debt), and high cash flow visibility

- Investors with a 5-7-year horizon

- Investors who want to invest in a high quality small & midcap portfolio.

If you would like to invest in mutual funds, reach out to us today!