In the Indian mutual fund landscape, there is a category of funds that is sitting at a crossroad. The category represents something specific: a systematic way to gain equity exposure while anchoring the portfolio in companies that have demonstrated the discipline to return profits to shareholders.

At the most fundamental level, a dividend yield fund is an equity mutual fund whose primary investment mandate is to build a portfolio of stocks with a higher-than-average dividend yield of the market. The dividend yield of a stock is simply:

Dividend Yield (%) = (Annual Dividend per Share / Current Market Price) × 100

So, if a company pays ₹20 per share annually and its stock trades at ₹500, the dividend yield is 4%. Dividend yield funds aggregate such companies — those that consistently generate enough free cash flow to distribute a portion of their profits to shareholders on a regular basis.

Fund managers in this category typically look for companies that satisfy a combination of criteria:

- Consistent track record of paying dividends (usually 3–5+ years)

- Dividend yield above the market average (often above the Nifty 50’s average yield of ~1.2–1.5%)

- Strong cash flows and manageable debt

- Stable business models — often in sectors like PSU banks, energy, FMCG, utilities, and established industrials

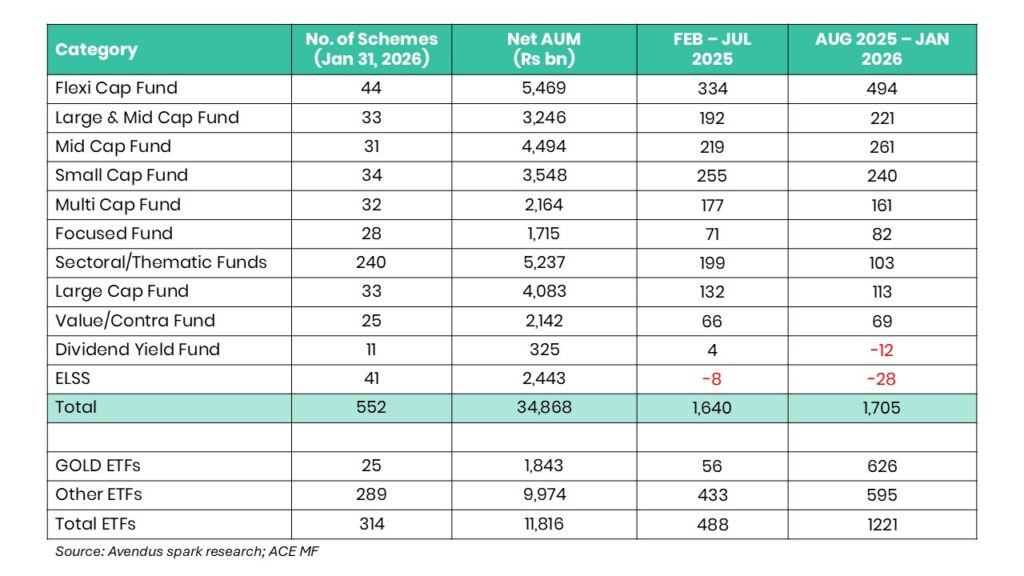

Low Investor Interest In The Past Year

Over the last 12 months, net inflows have been negative in most months, with outflows peaking at around Rs 300 crore in November and December 2025. Latest February 2026 numbers from AMFI (Association of Mutual Funds In India) though show a turnaround, with net inflows coming in at Rs 21 crore. What’s changing with the portfolios of dividend yield funds? Are they positioned for better times ahead?

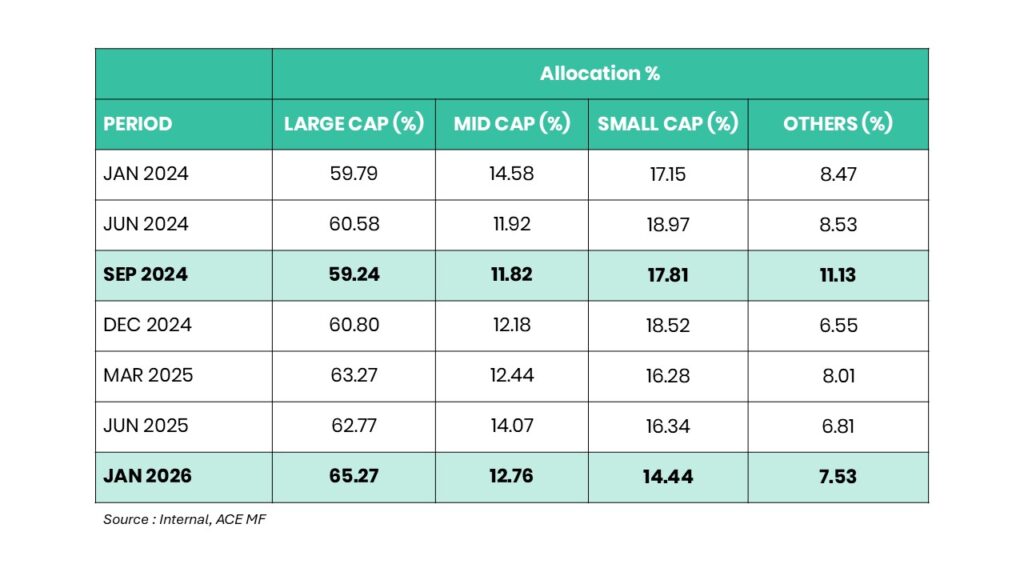

How Portfolios Looked Till 2024

Dividend yield funds were effectively multi-cap portfolios before SEBI recategorization came in in 2018.

For example, in January 2018, the category’s large-cap allocation was only 47%, with mid and small caps both around 21%. This helped in the performance of the category as the small cap rally boosted overall returns.

By December 2021, large-cap exposure jumped to ~62.5%, while small caps fell to ~12.6%, aligning closer to a portfolio of large-cap dividend stocks.

Then came the PSU rally. Through 2022, large-cap exposure climbed further to ~65%, helped both by fresh buying and the sharp appreciation in dividend-heavy PSU names. Funds like ICICI Pru Dividend Yield benefited significantly from this phase.

2023 saw another shift: small-cap exposure rose back to ~16%. Managers were either adding small-cap dividend names or benefitting from the broader small-cap rally, making it the second return driver alongside PSU large caps. The period between 2022 to 2024 was the strongest for the category.

However, the strategy is not without pain. The Nifty Dividend Opportunities 50 Index has historically seen >20% drawdowns in prolonged periods — notably in 2013, 2016 and again in 2024. Post 2024, with the market becoming more volatile, the repositioning has been slower, which explains the relatively muted catch-up in performance so far.

How Are These Funds Positioned Now?

Dividend yield funds are going through a structural repositioning, with large caps being the focus again.

Funds are now overweight private banks, IT, Autos and FMCG — largely private-sector driven exposures. Each scheme reflects the fund manager’s style, with some running high active share while others stay close to the benchmark.

The most aggressive positioning comes from ABSL MF ( Aditya Birla SunLife Mutual Fund), with nearly 30% allocated to IT and FMCG while staying significantly underweight banks. At the other end, the HDFC dividend yield fund sits closest to the benchmark, resembling what an investor might expect from a quasi-passive dividend yield strategy.

Dividend yield funds therefore sit in an interesting middle ground with enough flexibility to allow meaningful portfolio divergence.

From here, the winners will likely be the funds whose active sector bets re-rate over the next 12–24 months — Power for Franklin/Sundaram/Tata funds, FMCG for ABSL MF, and Finance/IT for UTI MF.

5 Takeaways For Investors

1. Dividend Yield Funds Are Not Defensive Income Funds

Despite the label, these funds have historically shown volatility, with drawdowns exceeding 20% in market cycles as mentioned above. Investors should approach them as thematic equity exposure, not as a low-risk income strategy.

2. The Category Is Currently Positioned Around Private-Sector Leaders

Most portfolios are now tilted toward private banks, IT, autos and FMCG, with selective exposure to PSU power and capital goods. Returns going forward will therefore depend on when these sectors re-rate over the next cycle.

3. Manager Style Matters More Here

Because the stock selection is based on dividend-paying companies, portfolio construction can vary widely across funds. Investors should pay attention to sector positioning and active bets, not just the category label.

4. Works Best As A Tactical Allocation

Dividend yield funds are best used as a complement to a core large-cap or flexi-cap allocation, rather than as a primary holding.

5. Suitable For Investors With A Medium-To-Long Horizon

These funds are meant for those investors who:

- Have a moderate risk appetite.

- Are comfortable with equity volatility

- Have a 3–5+ year horizon