When Raj came to us, he had ₹25 lakhs invested. And he had no idea if it was working for him. Here’s what we found — and what we did.

When Raj walked in….

Raj is 44 and a senior manager at a mid-sized manufacturing firm. One kid, a home loan in its fifth year, and a portfolio he had been building quietly for nearly a decade — one fund here, one tip there, a couple of ELSS investments around March every year and so on.

He wasn’t careless. He wasn’t uninformed. He just never had anyone sit down with him and help him look at the whole picture.

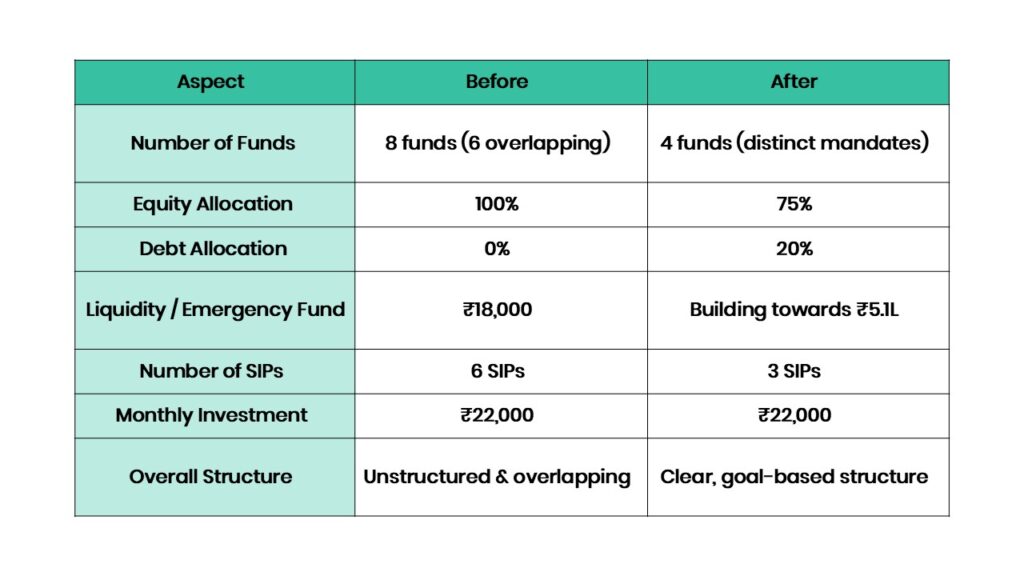

When he finally did, the picture was not what he expected. At the time of the audit, he had ₹25 lakhs across 8 funds, ₹22,000/month in SIPs, 16 years to retirement, two goals (retirement corpus and daughter’s education in 8 years), and a self-assessed moderate-aggressive risk appetite.

What the Audit Revealed

We ran a full portfolio review — holdings, allocation, overlap, tax history, and liquidity. Four problems jumped out immediately.

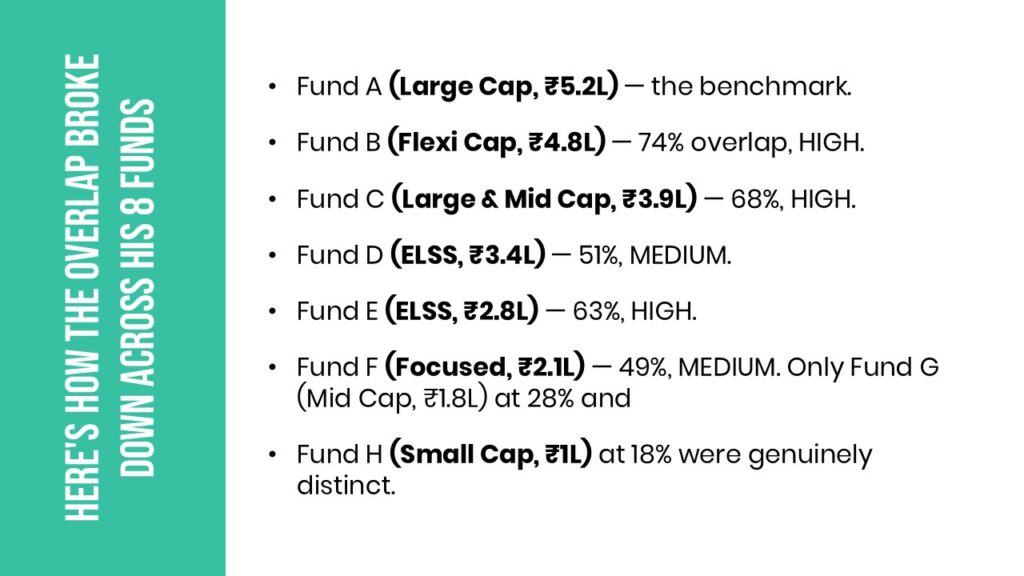

- FINDING 01 – 8 Funds (Effectively 2)

Raj thought he was diversified. He had 8 funds. But when we mapped underlying stock holdings, 6 of those 8 funds were investing in almost the same large-cap universe — for eg., Reliance, HDFC Bank, Infosys, ICICI Bank, TCS appearing repeatedly across funds.

Here’s how the overlap broke down across his 8 funds:

Six funds. Six expense ratios. Only one effective portfolio.

Funds A through F were largely duplicating each other. Raj was paying six separate expense ratios to hold what was essentially one large-cap portfolio.

“I thought having more funds meant more diversification. Nobody told me that’s not how it works.”

— Raj, during the first review session

- FINDING 02 – Zero Debt Instrument – At 44

At 44, with a 16-year runway to retirement, a 0% debt allocation is aggressive — not in the good way. A deep market correction of 30–40% (which happens every few years) could take longer to recover from, with no ballast.

Raj was 100% in equity. Zero debt, zero hybrid. The age-appropriate target for his profile was 75–80% equity and 20–25% debt — meaning roughly ₹5–6 lakhs of his portfolio should have been in stabilising instruments. It wasn’t.

Rule of thumb: More nuanced frameworks consider goals, income stability, and risk tolerance — but Raj’s 100% equity at 44 especially with daughter’s education goal coming up in 8 years, needed some debt cushion.

- FINDING 03 – No Emergency Fund

Raj had ₹25 lakhs invested. He had ₹18,000 in his savings account. His monthly household expenses were approximately ₹85,000.

Monthly expenses: ₹85,000. Six-month buffer needed: ₹5,10,000. Liquid savings on hand: ₹18,000. Shortfall: ₹4,92,000.

If a job loss or medical emergency had hit, Raj would have had no choice but to redeem equity funds — and if unlucky, at the worst possible time. That’s exactly the situation an emergency fund exists to prevent.

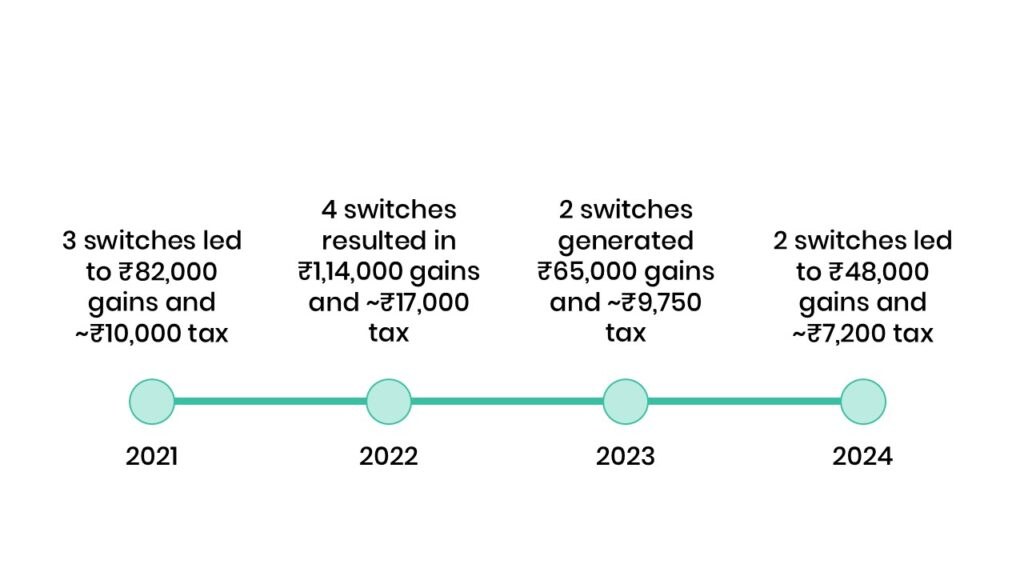

- FINDING 04 – A Costly Switching History

When we pulled Raj’s transaction history, we found 11 fund switches over 4 years — most triggered by news cycles, WhatsApp forwards, or a fund going through a rough quarter. Each switch had tax implications he had never accounted for. Over four years, Raj made 11 switches — almost none of them for the right reasons. Most of these redemptions happened within one year, meaning the gains were largely treated as short-term and taxed at 15%, with limited benefit from the ₹1.25 lakh annual LTCG exemption.

In total, this resulted in ₹44,000+ of avoidable tax leakage — without any meaningful improvement in portfolio performance.

The Conversation with Raj

We didn’t walk in with a prescription. We walked in with questions.

Why did he pick these funds? What was his plan when markets fell 30%? Had he ever thought about where his daughter’s college fees would come from if markets were down in 2032? Raj is sharp. Once he saw the overlap analysis, the debt gap, and the switching tax math — he got it. The problem wasn’t his intent. It was the absence of a structure.

We then built the restructured plan together — not handed to him, built with him. That matters. A plan Raj understands is a plan Raj will stick to.

The Restructured Portfolio

The goal: simplify, add stability, build liquidity, and stop the tax leakage. Here’s the before-and-after at the allocation level.

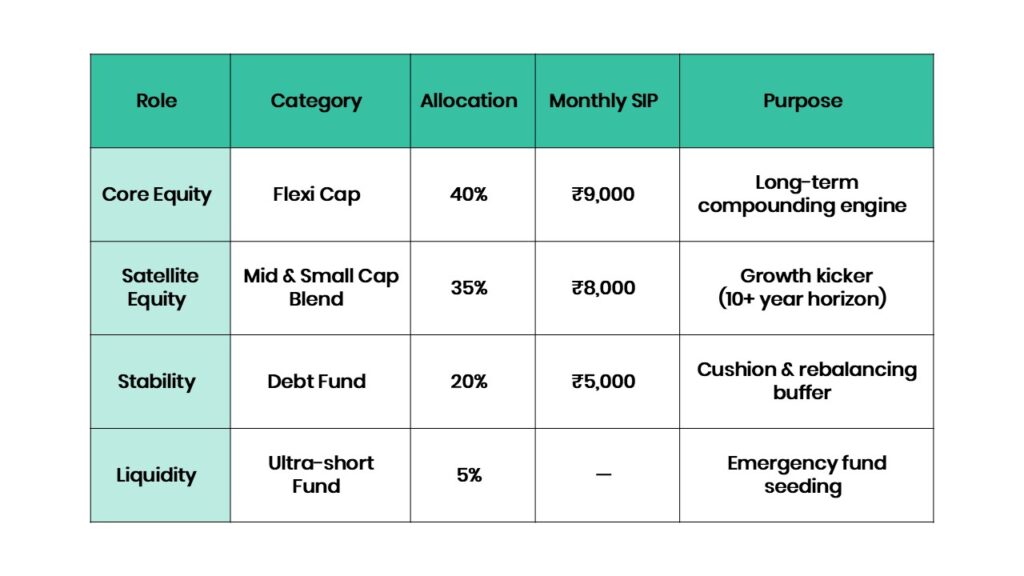

The New Fund Structure

The Switching Plan — Done Carefully

We didn’t switch everything at once. Overlapping funds were redeemed in tranches over two financial years to manage tax incidence. Long-term holdings (over 1 year) were prioritised for redemption first to attract LTCG rates instead of STCG. Redemptions were staggered across two financial years to keep tax low. Long-term holdings went first:

Fund B (3.2 yrs, ₹1,42,000 gain) → LTCG → ~₹4,200 tax (post utilisation of ₹1.25L exemption across other redemptions in the same FY)

Fund C (2.8 yrs, ₹98,000 gain) → LTCG → nil (within exemption)

Fund E (1.2 yrs post lock-in, ₹61,000 gain) → LTCG → nil

Fund F (0.9 yrs, ₹29,000 gain) → STCG → ₹5,800 tax

Total restructuring tax: ~₹10,000. Compare that to the ₹44,000+ Raj had been paying through reactive switching.

Where Raj Stands Today

It’s been 14 months since the restructure. Here’s the update.

Fourteen months on: portfolio up from ₹25L to ₹29.4L. Emergency fund at ₹3.2L, on track for ₹5.1L. Active funds: 4, with zero overlap. Reactive switches since restructuring: 0 — versus 11 in the four years before.

The portfolio went through a market correction of ~11% in this period. Raj did not call in panic. He did not switch funds. The hybrid allocation cushioned the drawdown, and he stayed the course.

“Earlier, every time the market fell, I’d open my app and feel sick. Now I know what each fund is supposed to do. I actually stopped checking daily.”

— Raj, 14 months after restructuring

What This Story is Really About

Raj didn’t have a bad portfolio because he made bad decisions. He had a bad portfolio because no one had ever helped him make a coherent one.

The problem with do-it-yourself investing isn’t motivation or discipline. It’s the absence of a framework — something that connects your money to your actual life, not just to a list of top-rated funds.

₹25 lakhs is not a small amount. It deserved a structure. Now it has one.

Key Lessons from Raj’s Audit

- More funds ≠ more diversification. Overlap is the real risk.

- Every year without debt at 40+ is a year of unhedged exposure.

- An emergency fund is not optional — it’s what lets you stay invested when markets fall.

- Reactive switching is a tax problem as much as a returns problem.

- The best portfolio is one you understand well enough to hold through a correction.

If you wish plan your finances better, understand whether you are on the right track, or review your goals and investments, reach out to us today !