Walk into any tier-2 city in India today and look around. The streets are lined with branded stores, the malls are buzzing, app-based food delivery is in full swing , and smartphones are in nearly every pocket. India, quite simply, is consuming — and it is consuming more with every passing year.

Over 60% of India’s GDP is driven by domestic consumption — making the country the world’s third-largest consumer market. The latest Economic Survey 2025–26 put an even finer point on it: the share of private final consumption expenditure rose to 61.5% of GDP in 2025–26 — the highest level since 2011–12.

The fact that consumption is driving the economy is not a coincidence or a cycle. That is the architecture of the economy itself. Here’s what data available in the public domain show :

1. Demographics Are on the Side of the Spender

India’s median age is around 28 years The country’s working-age population (15–64 years) is set to reach 100 crore by 2030, making up one-fifth of the global workforce. Young workers mean more earning, more spending, and more aspiration. This demographic dividend is not a 5-year story. It is a 25-year structural tailwind.

2. Premiumisation Is Reshaping Every Category

The Indian consumer is no longer just looking for cheap, good-looking and durable. Spending habits now reflect status, self-care, and experience. Premium skincare, organic food, branded apparel, luxury apartments in tier-2 cities — this premiumisation wave is powering higher revenue and better margins across FMCG, automobiles, retail, and consumer durables.

Around 40% of Indian consumers are already willing to pay a premium for health and wellness products — compared to the global average of just 29%.

3. Rural India Is Growing Strong

The consumption story is no longer limited to Mumbai and Bengaluru. Rural India is catching up fast. By 2031, rural areas are expected to contribute 55% of incremental consumption growth. Better roads, rural electrification, digital payments via UPI, and rising agricultural incomes are bringing the Bharat consumer firmly into the picture.

4. Digital Stacks Are Supercharging Growth

With 659 million smartphone users and UPI transactions crossing ₹23.48 trillion in a single month (January 2025), India’s digital infrastructure has unlocked consumption in markets that were previously unreachable. E-commerce, quick commerce, and D2C brands are bringing premium products to tier-3 towns — and finding ready buyers.

5. Policy Tailwinds Are Actively Fuelling Demand

The Union Budget 2025 exempted individuals earning up to ₹12 lakh annually from income tax — directly benefiting 75% of the salaried middle class. The government has also made major pushes in affordable housing, rural employment, and healthcare subsidies. Meanwhile, proposed GST rationalisation further puts more money into consumers’ wallets.

For investors, these factors raise a very important question: should you be putting your money in India’s growth story through consumption funds?

Consumption funds

Consumption mutual funds are thematic or sectoral equity funds that invest primarily in companies that benefit from rising consumer spending in India. Under SEBI’s framework, these funds must allocate at least 80% of their portfolio to companies aligned with the consumption theme.

This typically includes companies across:

- FMCG — eg. Hindustan Unilever, ITC, Nestle India, Britannia

- Automobiles — eg. Maruti Suzuki, Bajaj Auto, TVS Motor

- Retail — eg. Avenue Supermarts (DMart), Trent, V-Mart

- Consumer Durables — eg.Havells, Voltas, Titan, Asian Paints

- Hospitality & QSR — eg. Indian Hotels, Jubilant Foodworks

- Media & Entertainment — eg. Zee Entertainment, PVR Inox

The idea is simple: instead of picking individual consumer stocks, the fund manager does the job for you, constructing a portfolio across the consumption ecosystem — from the staples you buy daily to the aspirational purchases.

Performance

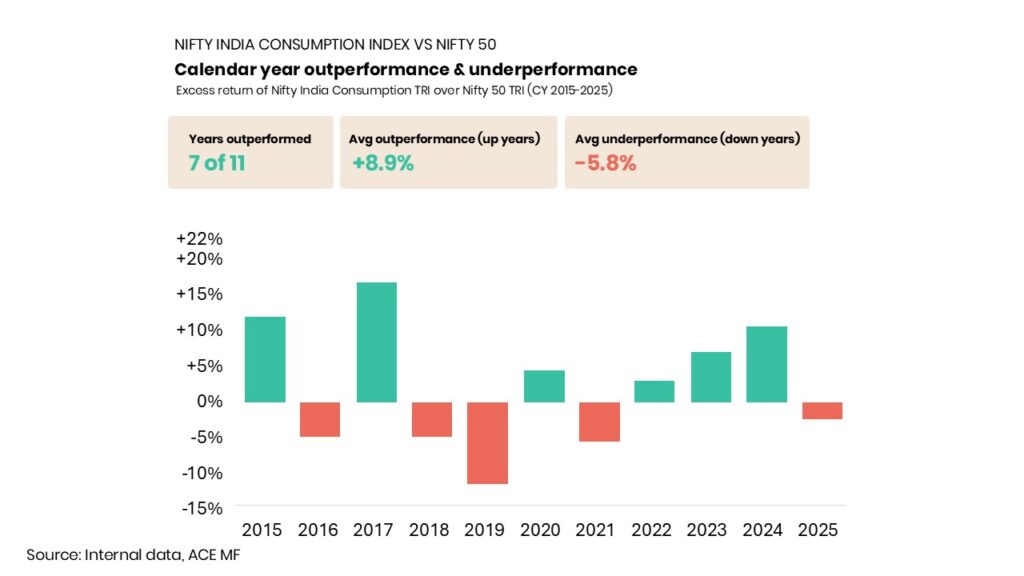

The most powerful takeaway from the accompanying infographic is that in 7 out of the last 10 years, Nifty India Consumption index has outperformed the Nifty 50 Index by an average of 8.9%. The recent 3-year streak (2022–2024) is significant, reflecting a structural shift post-Covid. India consuming more deliberately, premium-ising faster, and with more digital access than ever before.

Even otherwise, none of the underperformance years were random. Each had a specific, identifiable cause — and in every case, it was a credit disruption or demand shock, not a structural failure of the consumption theme:

• 2016 — Demonetisation froze cash-dependent consumption overnight

• 2018 — IL&FS crisis tightened consumer credit across the board

• 2019 — NBFC collapse crushed rural credit and demand

• 2021 — The second COVID wave hit discretionary spending hard

• 2025 — Urban consumption slowdown amid global uncertainties

This pattern has an important implication for investors: consumption underperforms during credit shocks and demand disruptions but delivers stable outperforming returns over longer periods.

Consumption funds are not for every investor in every situation. There are approximately 26 equity consumption mutual fund schemes in India. There are 3 kinds of funds in this category:

Type 1 — New Consumer Bulls (Mirae, ICICI Pru funds) These funds define consumption broadly to include digital platforms, consumer finance, and healthcare alongside traditional FMCG. They are making the explicit bet that India’s next consumer wave will be driven by credit penetration, digital commerce, and wellness spending — not incremental FMCG volume growth.

Type 2 — Old Economy Consumer (ABSL, Canara Robeco funds) These funds stay anchored to the classical consumption universe — FMCG staples and consumer brands with pricing power, quality management. They are underweight on auto, digital, and finance. They perform best when inflation and global uncertainty drive rotation from cyclicals to defensives — eg. periods like 2022 when FMCG dramatically outperformed.

Type 3 — Cyclical Consumer (Tata, SBI funds) Tata is explicitly auto-heavy; SBI is benchmark-tracking with mild tilts. These funds tend to outperform during economic expansion (2021–2023) and underperform during slowdowns.For example, the Tata fund’s 3-year leadership is a direct consequence of the auto supercycle; sustainability of that leadership into 2025–26 is questionable given auto earnings are decelerating.

Suitability

For those with the right horizon and risk appetite, these funds can be a powerful addition to their portfolio.

Consumption funds suit :

- Investors who believe in India’s long-term growth story and want focused exposure to it

- Those with an investment horizon of 5 years or more (thematic funds need time to play out)

- SIP investors looking to ride India’s consumption wave.

Who should be cautious:

- Investors who cannot stomach short-term volatility — consumption funds can underperform during economic slowdowns.

- Those who are new to equity investing

- Investors with lower risk appetite

The bottom line

India’s consumption story is not a trade. It is a structural mega-trend — built on demographics, aspiration, and a rising middle class that is only getting started.

For an investor who understands all of this, consumption funds offer a clean, professionally managed way to participate in this story — without the complexity of picking individual stocks or the unpredictability of cyclical sectors.

If you wish to participate in India’s growth story through mutual funds, reach out to us today !