Do you ever feel like you have worked so hard, but your money is gone as soon as it arrives? Where does it all go? – EMI for cars, home loans, and other gadgets, but although this gives you relief in the short term, it drastically slows down your path to achieving financial freedom.

What if the same monthly amount could grow your wealth? It’s possible by switching EMIs to SIP. In this blog, let me show you how the same money can work for you through SIPs by building assets instead of liabilities.

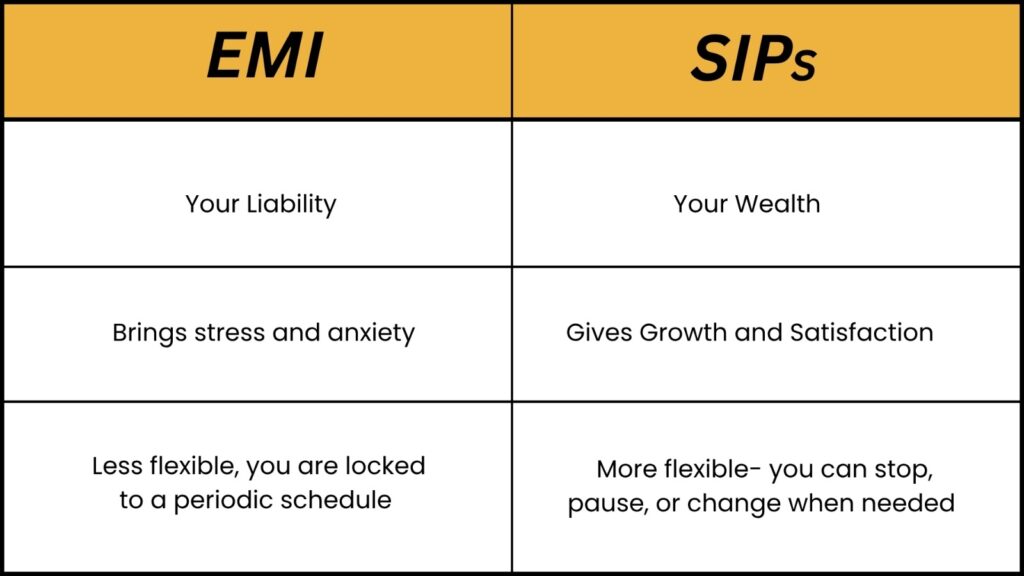

EMI vs SIP

Think of it like this, EMI is money going out of your pocket every month, whereas an SIP is like putting money in your pocket every month for your future growth

In this table, we can see the key differences between the two:

Let us explain the key differences using simple examples with two scenarios:

Scenario 1: EMI

Monthly EMI: ₹5,000

Tenure: 3 years (36 months)

Total amount paid: 5,000 × 36 = ₹1,80,000

After 3 years, you get the ownership of your asset ( Bike ), but what you can see here is, the depreciating asset may lose value over time very quickly. Even bikes lose 50% of their value, mostly in the first 3 years of purchase. So, your asset value will be Rs. 80,000 to 1,00,000.

Scenario 2: SIP Investment

Monthly SIP: ₹5,000

Tenure: 36 months

Assuming average annual return: 12%

Total amount invested: 5,000 × 36 = ₹1,80,000

The estimated value after 3 years will be ₹2,20,000 due to compounding growth.

Net outcome will be ₹2,20,000 asset grows substantially.

Why is this Shift Needed?

Why do we choose EMI? The answer is simple, we think it makes our life easier, but actually, it makes your life dependent. Meanwhile, SIPs will do the exact opposite; they give you control, discipline, and make your life independent by achieving financial freedom in the long term.

This shift is not only financial, but also psychological.

How to Start the Transition?

Now, you might be thinking that this all sounds great, but how do I actually start the transition? Here I will tell you some of the things you can try out.

- List down all your existing EMIs

Knowing is the first step to control, like where your money goes in the car loans, home loans, or some gadgets.

- Redirect to SIP

When one EMI closes, don’t let the money go into buying some other things which are unnecessary. Just steer it towards SIPs. That way, your spending habit will turn into a savings habit

- Stay consistent

Once you start the investment journey, don’t stop or pause in between. Let your money grow consistently and build solid wealth for you in the Long term with the power of compounding.

- Define Financial Goals

When your investments have a clear purpose, it’s easier to stay consistent. Your goals can be short-term, like a vacation or buying a gadget, or long-term, like your child’s education or early retirement. A clear goal keeps you motivated to invest regularly.

- Automate your investment

Just like your EMIs are auto-debited every month by the bank. You can set up your SIPs also to auto–invest. That really helps you never forget or skip the investment.

- Increase Gradually

Whenever your income goes up, you receive a bonus, or an EMI ends, don’t let that extra money slip away. Just increasing (step up) your SIP by 5–10% every year can make a huge difference in the long run. This is very important to reach your long-term goals faster.

Conclusion

EMI gives you short-term satisfaction, but SIP offers long-term peace of mind. So, every time you plan to buy a new product, pause a moment and think if it’s really worth buying it now or if I can put this money into a SIP? One choice throws you into debt, and the other builds wealth; the decision is in your hands.